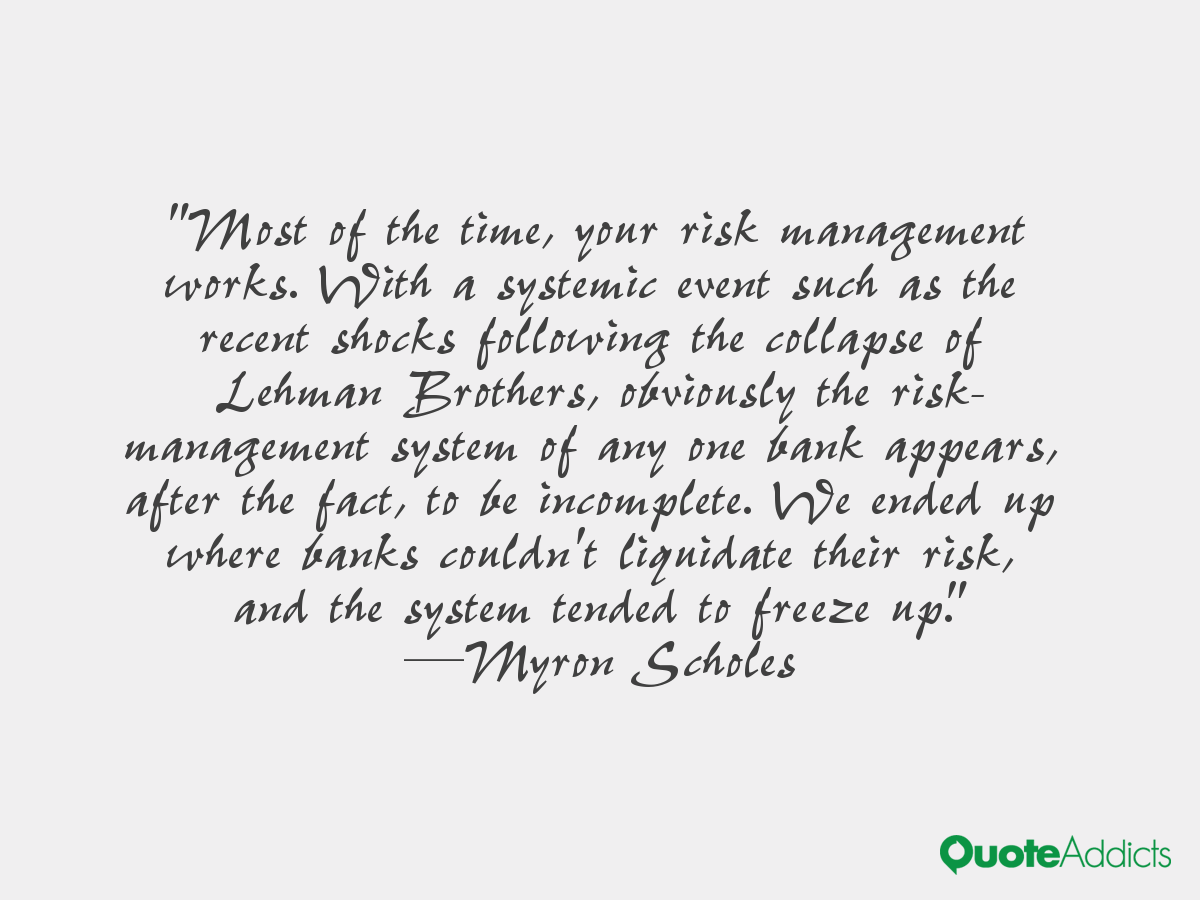

Myron Scholes Quotes

Myron Scholes — Canadian Economist born on July 01, 1941,

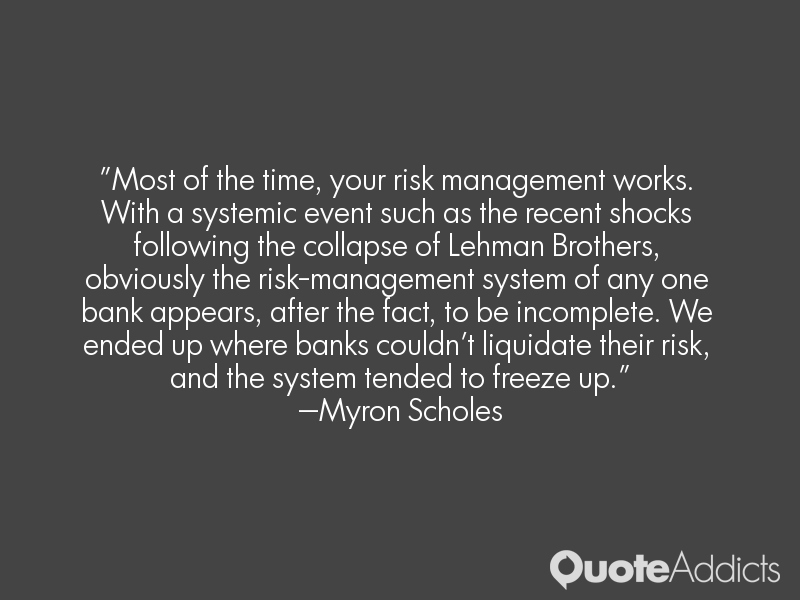

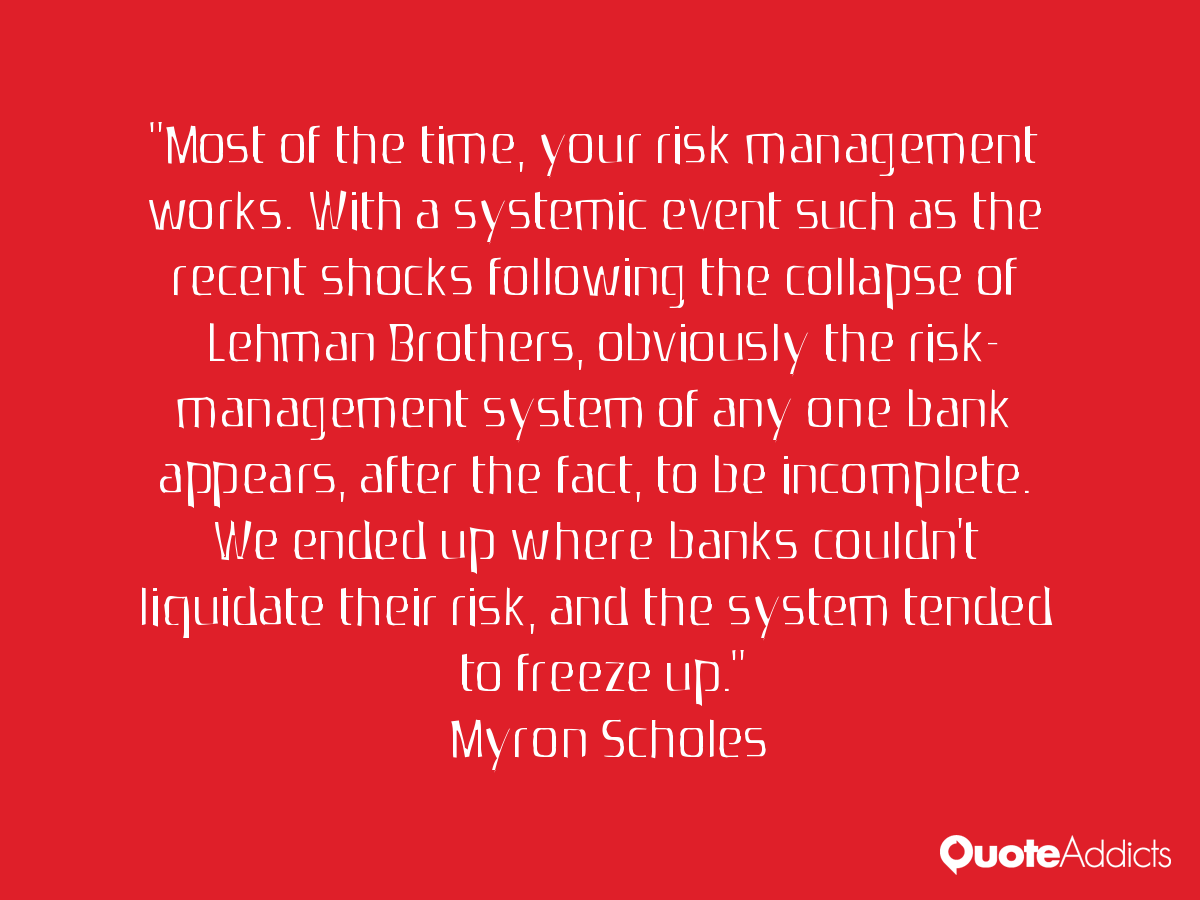

Myron Samuel Scholes is a Canadian-American financial economist. In 1997 he was awarded the Nobel Memorial Prize in Economic Sciences for a method to determine the value of derivatives. The model provides a conceptual framework for valuing options, such as calls or puts, and is referred to as the Black–Scholes model. Together with fellow Nobel prize winner Robert C. Merton he founded the hedge fund Long-Term Capital Management which dramatically collapsed in 1998... (wikipedia)